Explore the different types of Australian bank accounts, their features, and benefits to help you choose the perfect one for your financial needs.

Are you looking to manage your everyday expenses, grow your savings, or perhaps set up something that fits your business needs?

Each bank account type in Australia has its own features, benefits, and, most importantly, fine print.

This guide will walk you through the essentials of Australian bank accounts, breaking down the different types and their perks.

From everyday accounts designed for quick transactions to savings accounts that help your money grow, we’ll help you find the account that best aligns with your financial goals.

Ready to get started on simplifying your banking choices? Let’s begin, then!

In Australia, most bank accounts fall into two broad categories: Everyday (Transaction) Accounts and Savings Accounts.

Each one has a different purpose, so understanding the differences helps you choose the right one.

Everyday accounts are your all-purpose accounts for managing day-to-day expenses, like paying bills or grabbing a coffee.

They’re designed for frequent transactions, so you can easily access your money whenever you need it. Here’s what to know:

📌 Did you know?

According to SECNewgate research, only a small percentage of account holders know their exact interest rates for transaction (14%) and savings accounts (20%), but more are aware of term deposit rates (43%).

In Australia, an everyday banking account (also called a transaction account) is used to manage your daily expenses, like paying bills.

In other countries, you might hear this type of account referred to as a current account (UK) or a checking account (US), but the purpose is essentially the same: it's a flexible account for everyday use.

Understanding these different terms can help when comparing banking options internationally.

If your goal is to build up your savings, a savings account is the better choice. These accounts are designed to help you earn interest and accumulate funds over time.

Here are the main types:

1. Standard Savings Accounts:

These are the most basic options. You earn a modest interest rate and have easy access to your money, making them simple and straightforward.

2. High-Interest Savings Accounts:

If you’re looking for better returns, these accounts offer higher interest rates. However, there’s often a catch – like restrictions on withdrawals – to maintain the higher rate. Think of it as a way to encourage you to let your money sit and grow.

3. Round-Up Savings Accounts:

Round-up savings accounts help you boost your savings while using their debit cards for everyday purchases. These accounts are linked to your transaction card and automatically round up each purchase to the next set amount you choose, such as the nearest dollar, $2, $5, or $10.

The difference between the purchase price and the rounded-up amount is then transferred directly into your linked savings account.

For example, if you make a $12.75 purchase and have chosen to round up to the nearest $5, the total amount debited would be $15. The extra $2.25 would be transferred to your savings account, while $12.75 covers the actual purchase.

4. Bonus Savings Accounts:

These accounts offer extra interest if you meet specific conditions, such as making regular deposits without taking any money out. It’s like a small reward system for good saving habits.

5. Term Deposits:

This option locks your money away for a fixed period (ranging from a few months to several years) in exchange for a higher interest rate. However, withdrawing your money early usually comes with penalties, so it’s best for those who don’t need immediate access to their funds.

📌 Did you know?

Data from the research we mentioned shows that almost all Australians hold a transaction account (95%), and savings accounts are also common (79%).

In contrast, only 19% have a term deposit, and 13% hold cash management accounts.

Also, about a third of Australians have searched for a new transaction or savings account in the last three years, mainly to find better interest rates.

Beyond the basics, there are a few specialised accounts available that cater to specific groups or situations:

Selecting a bank account isn’t exactly a one-size-fits-all situation. Here’s how you can ensure you make the right choice without feeling like you’re solving a mystery:

First things first – why are you opening an account? Is it for everyday expenses, building up savings, or managing business finances? This saves you from opening three different accounts when one specialised one could do the job.

Fees are like the fine print on a contract – easy to overlook, but they can bite.

Monthly fees, ATM charges, or transaction fees can add up over time, eating into your funds. Many banks offer no-fee options if you meet certain criteria, so dig into the details.

Ask yourself: Will I be able to meet these conditions, or is the fee-free dream too good to be true?

If you’re opening a savings account, interest rates should be your main focus.

Compare different accounts and make sure you’re getting the best return for your hard-earned cash.

📍 Pro tip:

Pay attention to the conditions attached. Sometimes, a ‘high interest’ account only gives you the best rate if you jump through hoops like depositing a specific amount each month or avoiding withdrawals.

How easily can you access your funds? Some accounts offer fantastic online banking features, while others might charge you for ATM withdrawals.

If you’re the type who likes to check their balance on the go or make spontaneous purchases, prioritise accounts that offer excellent mobile banking and low ATM fees.

⚡Don’t miss out on our guide on How to open a business bank account in Australia!

Once you’ve chosen your ideal account, it’s time to optimise it. Here are some pro tips:

Choosing a bank account doesn’t have to be overly complex. The key is understanding what each type offers and aligning it with your financial goals.

In case you’re after an account that’s easy to access for everyday use or one that’ll grow your savings over time, there’s something out there for everyone.

Remember, bank accounts are tools to help manage your money, not mysterious entities. Approach them with a clear understanding of your needs, and you’ll avoid common pitfalls.

But what if you’re looking to take things a step further, like setting up a business account and managing a business seamlessly?

Imagine getting your company registered and setting up a business bank account, all in a few easy steps – no more jumping through hoops or dealing with complicated paperwork.

With ANNA, you can handle everything from securing your Australian Company Number (ACN) and registering your business name, to sorting out your ABN and GST, all in one place.

But it doesn’t stop there. The real game-changer is ANNA’s business bank account feature, which goes beyond basic banking.

Plus, ANNA’s virtual and credit cards mean you’ve got everything you need to keep your business running smoothly, while automatic tax reminders ensure you never miss a deadline again.

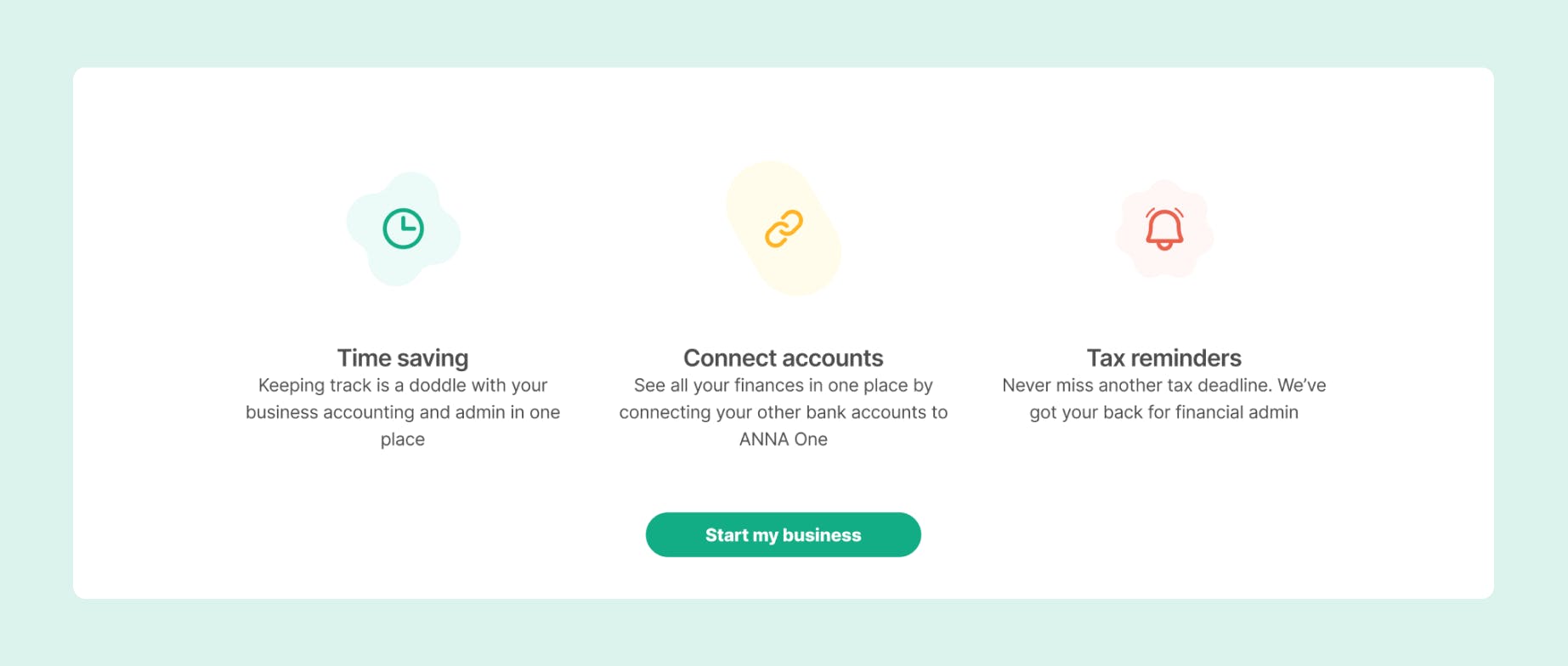

It’s like having a personal assistant for your finances – you can also automate your bookkeeping, send out invoices (and even chasing payments), and keep track of your expenses effortlessly.

With ANNA One, you don’t just have a bank account; you also have a complete financial toolkit that helps you manage your business with ease and confidence.

Say goodbye to paperwork and hello to running your business hassle-free!

Sign up now and set your business up for success!

Open a business account with ANNA and start sending and accepting payments today

Open a business account

.svg)